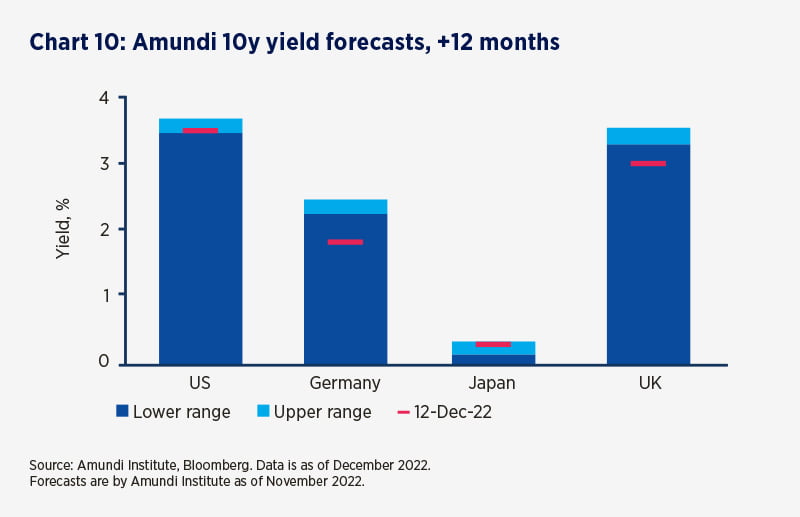

After the strong sell-off in government bonds amid volatile moves and factoring in tighter monetary policy, we believe core government bonds are already good value. At this stage, most of the expected tightening is already reflected in current yields, especially for US rates.

The Fed is maintaining its focus on controlling inflation, which is causing a decline in the possibility of a ‘soft landing’ scenario but a US recession is still not our base case. While we are neutral on duration at the moment we could raise our stance depending on how far UST yields increase. We think the risk-reward of being cautious on duration is less compelling now than it was earlier because of emerging growth concerns.

In Europe, we are slightly cautious on duration as the government bond market is likely to remain under stress. We anticipate the ECB will raise rates by a further 125 bps, bringing policy rates to peak around 3.25% in 2023. Conflicting forces remain at play with the ECB committed to tackling inflation while EU governments’ fiscal support feeds inflation. We believe that better opportunities will materialise later this year when the ECB will head closer to its terminal policy rate.

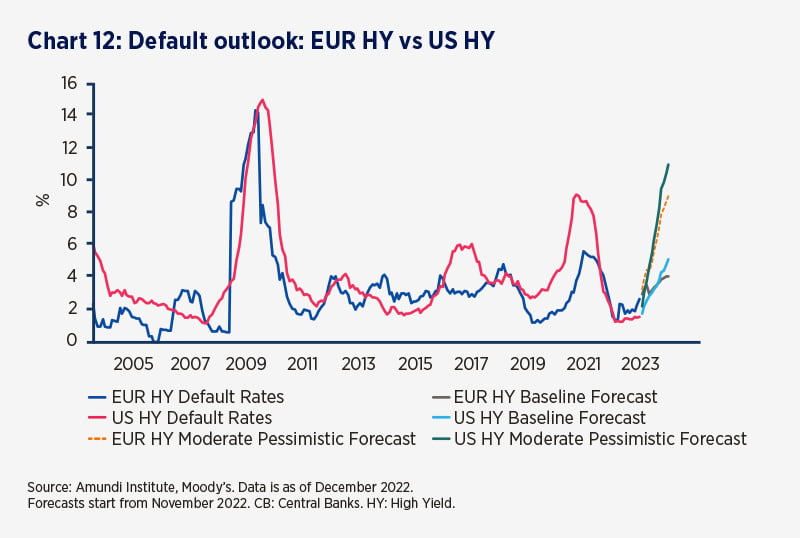

In terms of credit segments, we maintain a slight preference for IG credit, while being more cautious on risky assets such as HY. Over the next year, investors should closely monitor the impact of:

the slowdown in economic activity,

rising labour costs on margins and

policy tightening, especially on US corporates, paying attention to corporate leverage, and liquidity and refinancing risks.

In the US, the effect of monetary tightening on IG spreads has been limited so far. Companies currently have low refinancing needs and have dipped into their reserves for their funding needs, leading to reduced cash levels on balance sheets. These robust fundamentals coupled with a potential Fed pivot in 2023 make us positive on the asset class.

In the European corporate space, the inflation outlook, subsequent ECB policies and fiscal and energy policy will remain key drivers for corporate margins.

A new EU level fiscal support package could prove supportive of businesses and alleviate some of the economic fallout of tighter liquidity conditions and elevated energy prices. When allocating to corporates, we maintain a preference for high quality credit, and a bias towards shorter duration for the first quarter of 2023.

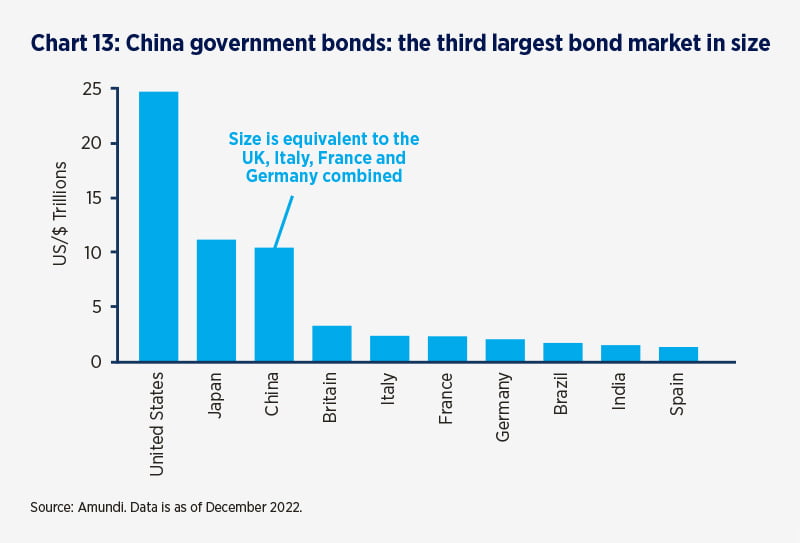

A dovish Fed pivot, a key driver for emerging market debt performance has yet to materialise, hence our cautious bias on EM debt in the near-term. Having said that, we believe entry points will materialise later in the year and we stand ready to reweight. Although the outlook for China remains uncertain, the PBoC recently provided additional support to the local debt market to ease stress levels and ultimately facilitate lending in a heavily disrupted economy. In addition, China’s gradual reopening, a dovish bias from the PBoC and the government’s signals for more support to growth may prove supportive for the market as the year progresses.China’s debt market, the third largest bond market in the world at USD 11 trillion, can offer an interesting source of diversification in a global fixed income allocation.