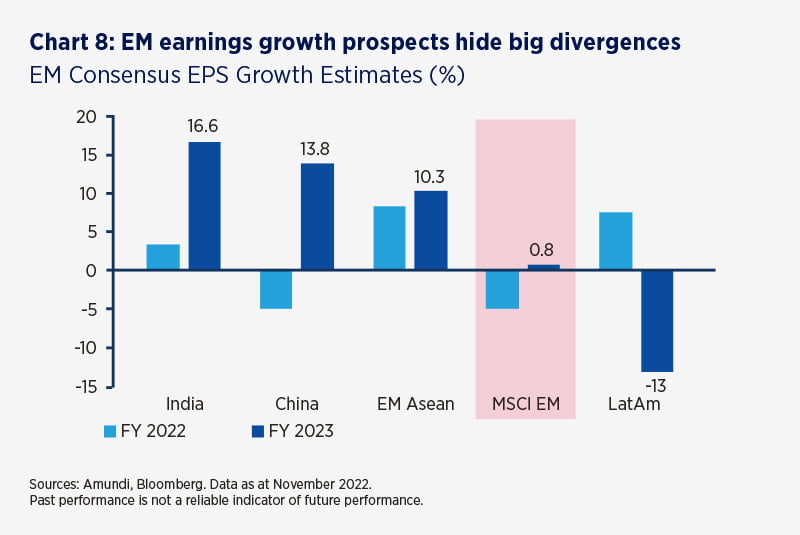

The performance of EM equities has been mixed since the beginning of last year. The significant underperformance of Chinese equities more than offset the strong performance of Latam equities, bolstered by their exposure to the commodity complex. Looking ahead, market expectations are for a small recovery in earnings growth in 2023.

Still, this aggregate measure hides strong divergences in the earnings outlook for individual countries / regions.

Our main convictions at country levels are Brazil, although we are assessing how the new President’s fiscal policies may impact public finances and economic growth; and the UAE.

In Asia, the Chinese economy is expected to rebound after the recalibration of the zero Covid policy but more clarity is needed. The strong decorrelation of Chinese equities performance to other markets, and the complexity of the local market, pushes for adopting a separate allocation to China from the EM block to reflect those divergences.

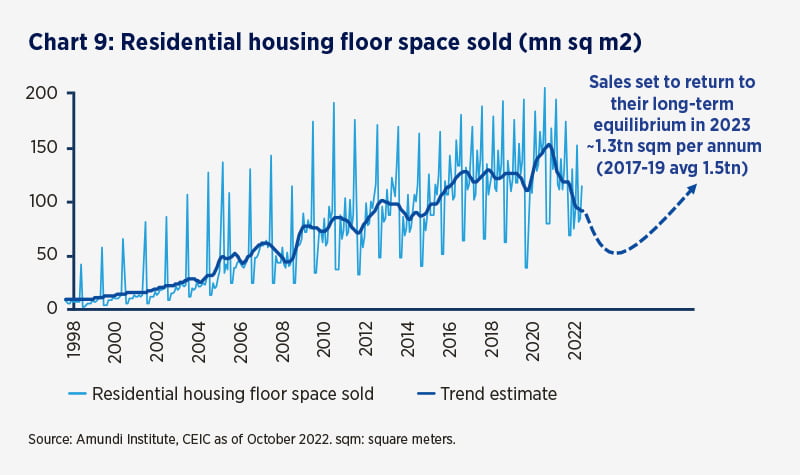

China’s economy has the potential to unveil positive surprises in 2023, depending on the outcome of two main challenges: the housing market and its Covid-19 policy. On the former, we see a stabilisation thanks to looser policy, on the latter a further relaxation of restrictions.

Newsflow has improved lately, with the Republic scrapping most of its controversial Covid controls (albeit resulting in a surge of Covid cases), leading to some recovery in asset pricing. Such actions have the potential to reduce the idiosyncratic risks that have hampered the performance of Chinese equities over the past year.

Regarding housing, the Q3 2022 PBoC survey showed that the share of households planning to buy homes increased for the first time since mid-2021. New home sales volumes, after seasonal adjustments, increased for the second consecutive month in September 2022.

Investors should stand ready to play the potential rebound later in 2023.

AMUNDI MSCI EMERGING EX CHINA ESG LEADERS SELECT UCITS ETF DR 0.35% OGC*