We believe that US equities should prove more resilient compared to other developed equity markets on the back of a relatively better inflation, economic growth and consumption backdrop.

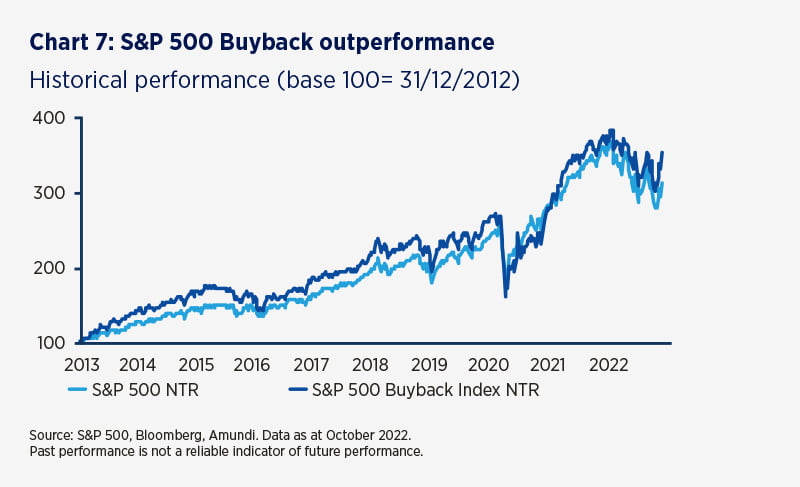

We have a preference for names that can reward shareholders by returning excess cash through dividends or buybacks, even in a difficult environment.

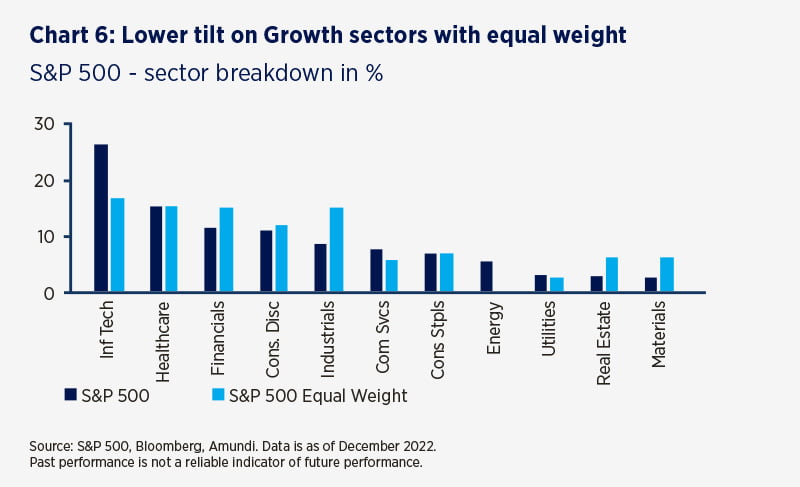

In a higher-for-longer interest rate context, we also favour lower exposure to growth stocks whose future earnings expectations can be negatively impacted by rising rates.

In addition, we have a defensive stance on mega-caps, which are also vulnerable in these conditions.

The S&P 500 equal-weight index bears a lower exposure to growth stocks and megacaps, compared to a market cap weighted index. By construction, it also exhibits higher dividend yields.

Recession risks are greater in Europe and the continent is likely to face a mild contraction in economic activity early this year. Elevated inflationary pressures are biting into corporate margins and the energy crisis triggered by the war between Ukraine and Russia adds to uncertainties.

In this environment, quality companies with high pricing power and high margin levels can more easily pass on rising input costs and may be better positioned to outperform.

A higher rate environment also tends to impact corporates with higher duration such as growth stocks.

On the other hand, corporates with greater earnings visibility and higher dividend payout policies may perform better in these conditions, hence our preference for value stocks and financials.

We also favour corporates with high payout policies that tend to have sustainable and relatively predictable cash flows.

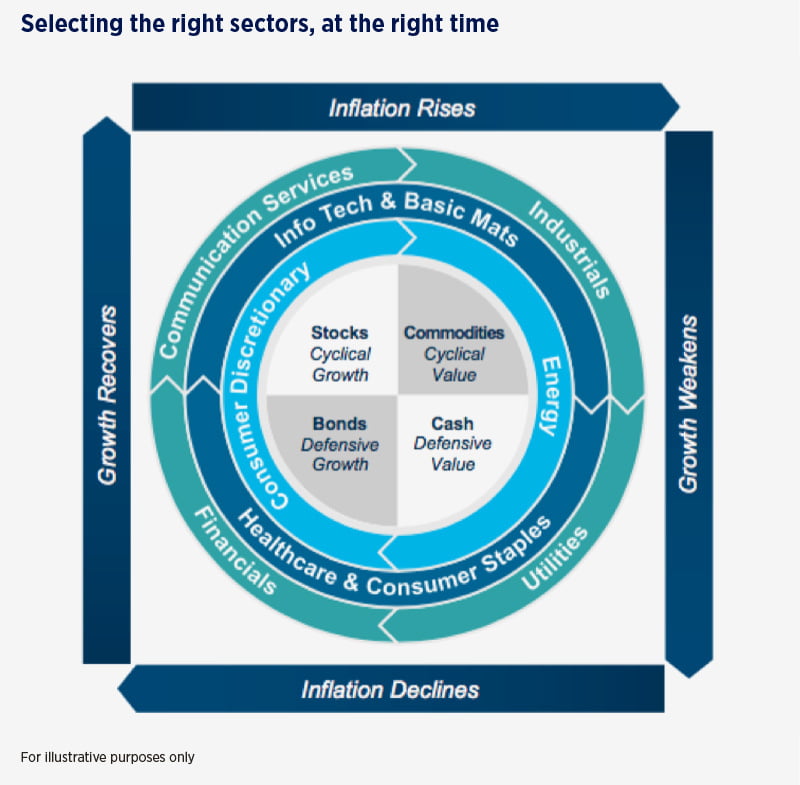

Incorporating a sector-based approach can help investors to adjust portfolio positioning according to their macro-economic views, investment objectives and risk tolerance. An agile sector allocation should allow investors to adapt their portfolio to each phase of the economic cycle.