The Great Repricing

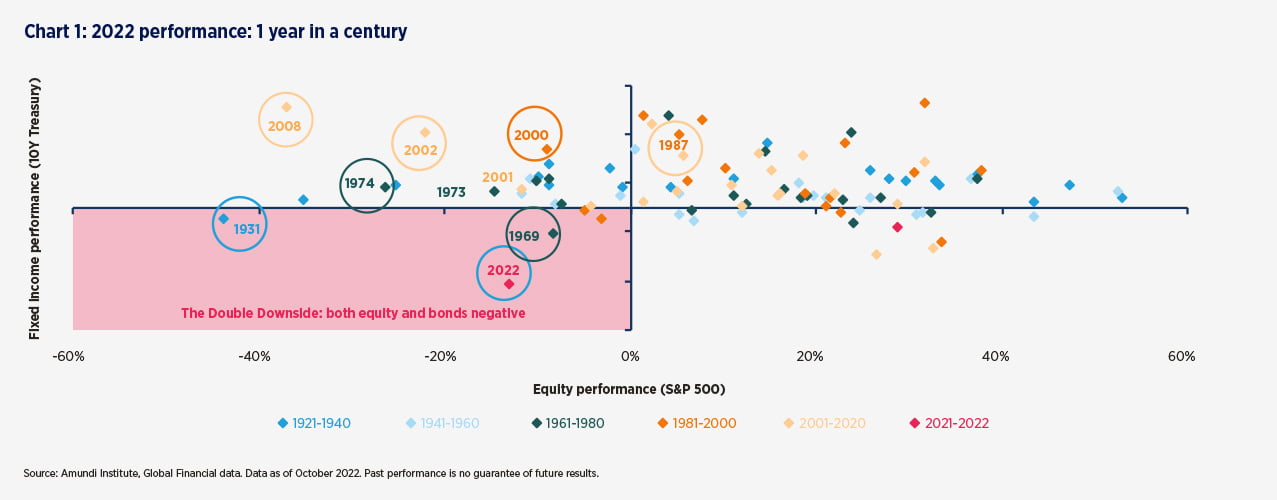

2022 was one of the worst years on record for multi-asset investors. Sustained inflationary pressures pushed central banks to embark on an aggressive pace of rate hikes. In this context, both equities and bonds experienced significant repricing. Bonds endured the worst annual performance in a century. Over the course of the year, the Federal Reserve (Fed) raised interest rates from 0- 0.25% to a target range of 4.25 - 4.50% — the highest level in 14 years.

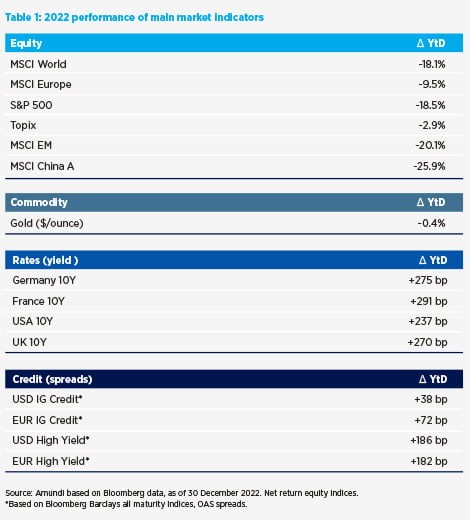

There was almost no place to hide across the year with all main asset classes in negative territory.

Oil, commodities and the USD were some of the only positive performers, making it difficult for investors to mitigate losses. With the USD, though, we are seeing signs of a change in the strengthening trend as the Fed lowers its rate hike trajectory, within an overall tightening stance.

Persistent inflationary pressures triggered by supply constraints, along with an energy shock aggravated by the geopolitical crisis, and rising interest rates affected the performance of both equities and bonds across 2022.

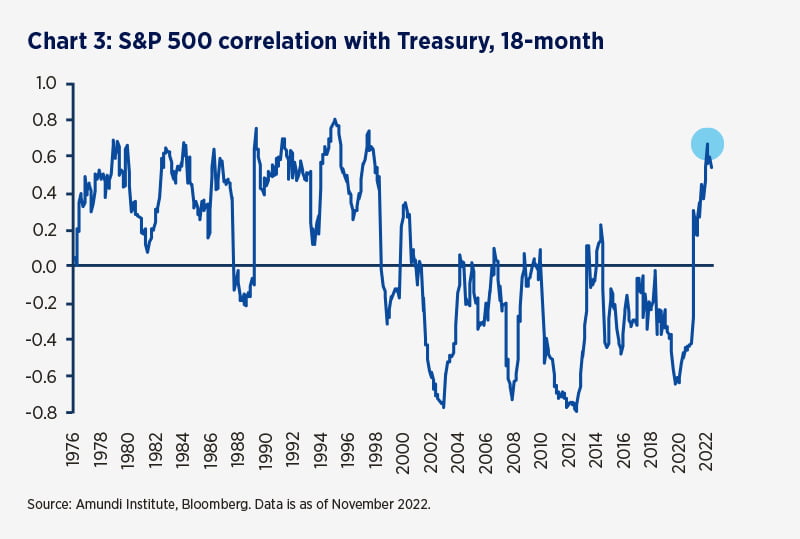

The correlation between both asset classes had already turned positive in September 2021 when central banks became more vocal on their policies to contain inflation. In 2022 market conditions drove the correlation even higher.

“There was almost no place to hide across the year with all main asset classes in negative territory.”

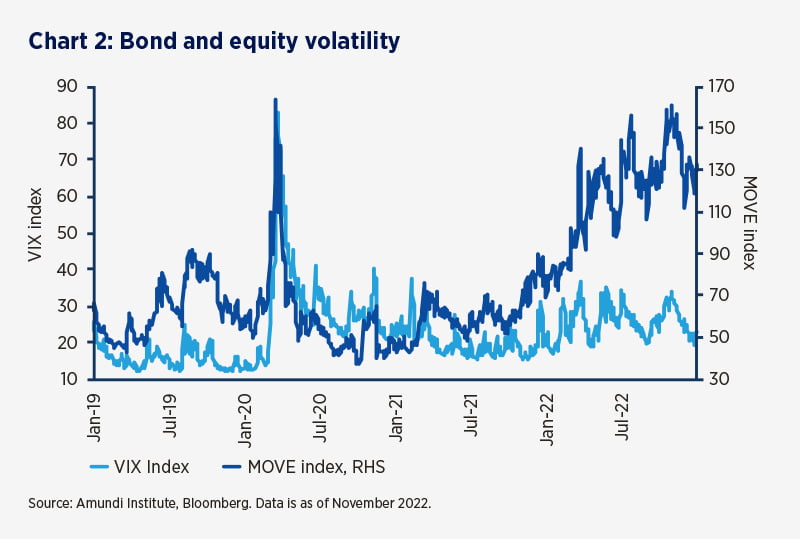

2022 was a volatile year with markets reassessing the impact on growth of persistent inflationary pressures and geopolitical risk following Russia’s invasion of Ukraine. Headline inflation in developed economies rose sharply, pushing central banks into an aggressive response at the risk of derailing the economic cycle.

The correlation between equities and bonds jumped to multi-decade highs. Government bonds bore the brunt of central banks’ aggressive response, while the hike in raw material prices also hit the performance of global equities.

The strong performance of growth-tilted US megacaps, which benefited the most from the pandemic, reversed and drove the strong under-performance of the S&P 500 within global equities.

Meanwhile, European equities suffered further downside with the emergence of the energy and cost-of-living crisis. Higher input prices bit into corporate margins and households’ disposable income.

The general rise in government bond yields also affected bond performance across the board. Still, lower duration exposures and defensive equities allocation proved the most resilient in the downturn. At a sector level, energy, basic resources and financials outperformed while industrials and retail sectors bore the brunt.

The performance of emerging markets was also mixed. Commodity exporters such as Brazil proved resilient, but this was more than offset by the strong underperformance of Chinese equities. Chinese activity was hit by strict pandemic curbs and deleveraging in the real estate sector, although towards the end of the year newsflow on economic reopening provided some cheer.

Finally, performance was also mixed for commodities. Oil and other energy prices were supported by the unfolding of the energy crisis triggered by the war in Ukraine. Gold prices were hit by the resurgence of positive real rates.

Explore the main market indicator performance in 2022 overleaf.

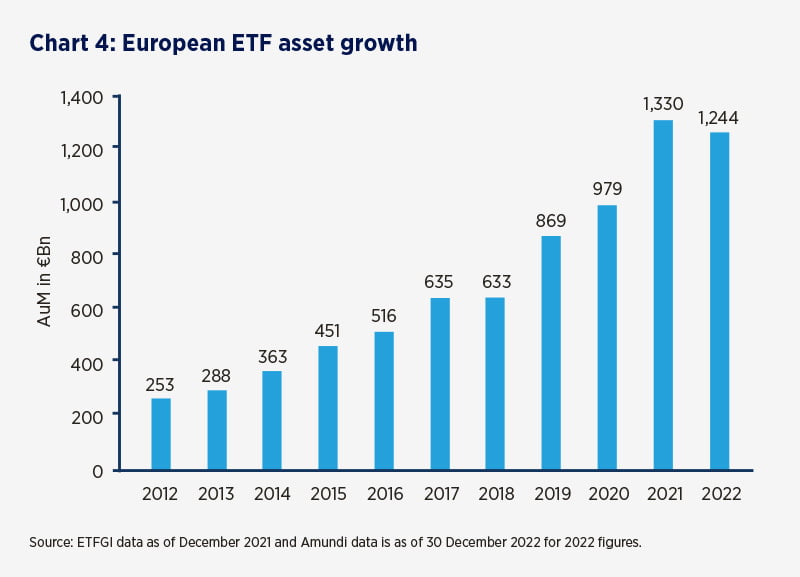

European UCITS ETF market experienced mildy negative growth in 2022 (-6.5%) with assets under management (AuM) reaching €1,244 billion versus €1,330 billion in 2021. It nevertheless displayed resilience in the face of difficult market conditions. Net new assets (NNA) were positive at €82 billion versus €158 billion in 2021. The decrease in AuM may be attributed to multiple factors including uncertainty over economic growth, the war in Ukraine, rising inflation and rates.

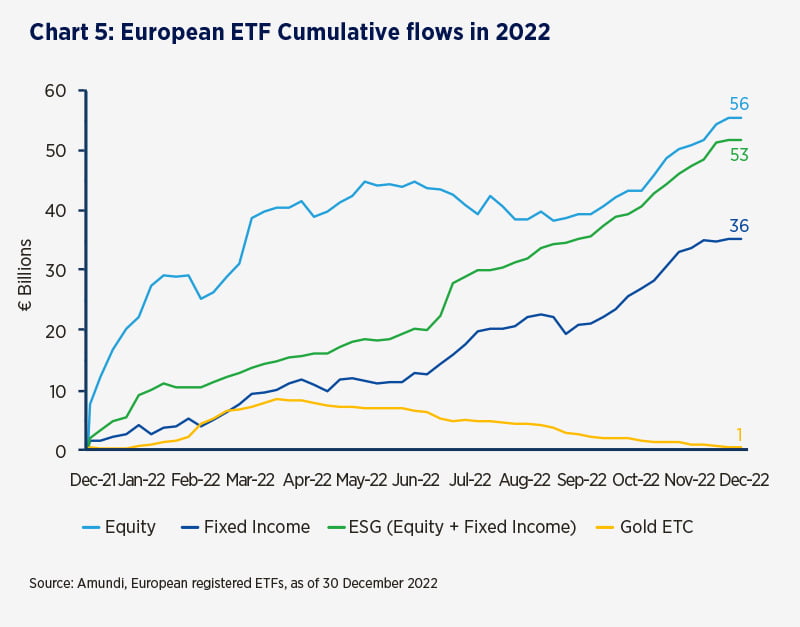

The rotation towards ESG remained strong in both equities and fixed income across the year. NNA reached €53 billion versus €87.7 billion for 2021. However, ESG ETFs accounted for 64% of total inflows in European ETFs (ex ETC) market (vs. 55% in 2021), demonstrating that the trend for sustainable investing continues to accelerate. In total, ESG accounted for 59% of equity net inflows (almost level with 2021) and c. 65% of all fixed income net inflows across the year (vs. 47% in 2021).

Total ESG ETF AuM in Europe continued to increase in 2022, standing at over €260 billion at the year-end and representing almost 21% of the total size of the European ETF (ex ETC) market.

At the beginning of 2022, investors were still in a risk-on mode but this transitioned to a more defensive stance following the outbreak of the war in Ukraine and mounting concerns over inflation and economic growth. NNA reached €56 billion at the year end versus €117 billion in 2021.

Eurozone equities suffered from almost €6.5 billion of redemptions whereas World Equities, US equities, All Country exposure and Emerging Markets gathered positive flows respectively.

Rising inflation was a major source of concern for investors in 2022 as reflected by inflows of more than €6.1 billion to inflation-linked products.

Upon inflation levels rising in the USA and Europe, investors redeemed inflation-related products to the tune of €5 billion. Chinese Government bonds, a popular investment theme in 2021 (attracting more than €7 billion), also suffered from large outflows in 2022 with €10.9 billion of redemptions. US treasuries drew investors at the beginning of the war in Ukraine as a flight to quality and then later in the search for yield following rate increases.

Patterns of flows to gold-tracking products followed an inversed V-shape in 2022. The onset of war in Ukraine led to the rise of uncertainties and flows to Gold ETC products reached €8 billion at end of April. Subsequently gold-tracking products suffered from steady outflows for the remainder of the year.

At the end of 2022 net new assets to gold ETCs reached €1 billion.