Thematics

Outlook: Thematic strategies, which focus on longer-term, global structural trends, are expected to gather even more momentum in 2024 and beyond.

Preferences: Consider megatrends such as robotics and artificial intelligence (AI), alternative energy and new energy technology, as supporting digital transformation and disruptive technology.

Thematics, also known as megatrends, are economic, environmental, social and technological forces reshaping the world for everyone, every day.

As uncertainty remains as a constant on global markets, these are long-term structural themes, which allows for diversification away from today’s biggest companies, which are systematically preferred by market-cap-weighted indices. Thematics can favour corporates that are ahead of a new millennial-led environment of green energy, digital transformation and disruptive technology, which can, in turn, provide portfolio diversification and potentially deliver returns in the long run.11

There are multiple trends supporting the growth of robotics and AI. From the automation of repetitive tasks to solving problems related to an aging population, to having multiple uses in agricultural technology and healthcare advancements. Robotics and AI also play a role in offering solutions to the climate crisis, by promoting efficient energy use and improved distribution.

The global robotics market is expected to reach 37 million units by 2025 – up from 12 million in 201912 – while the global AI market could reach $733.7bn by 2027, a CAGR of 42.2% between 2020 and 202713. With up to $15.7tn14 in economic value potentially added by 2030 from AI productivity, the investment opportunity is hard to ignore.

Amundi MSCI Robotics & AI ESG Screened UCITS ETFManagement fees 0.40%*

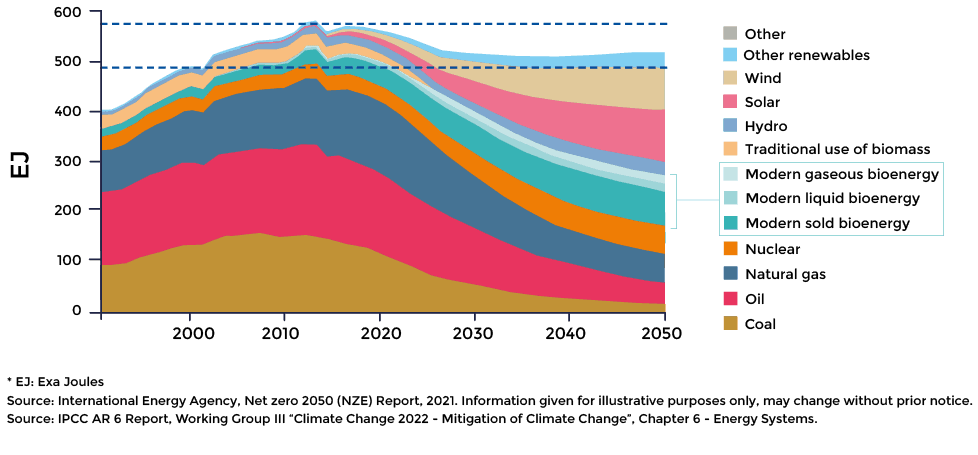

The global energy crisis has underscored the need to accelerate the energy transition. We believe the electricity sector will be the main contributor to emissions reduction in the net zero 2050 pathway.

In order to reach the 1.5°C limitation in warming, emissions reduction will rely on renewables, energy efficiency improvements, bioenergy with carbon capture and storage (CCS), hydrogen, and fossil fuels combined with CCS.

In 2021, the International Energy Agency (IEA) published its net zero roadmap, highlighting that investments in energy must rise from $2.3tn annually to $5tn by 2030 then $4.5tn by 205015. This creates huge investment opportunities for investors in companies which are exposed to alternative energy, energy efficiency and battery value chain.

Furthermore, investments into alternative sources of fuel, such as bioenergy and hydrogen, could be a high-value and large-scale mitigation option for sectors with limited alternative to fossil (aviation, heavy industry, chemicals)1:

Bioenergy is bound to strong growth: from one tenth of primary energy supply today to 18-22% in the 1.5°C scenarios in 205016.

Hydrogen is deemed by the EU to be critical in achieving its objectives of reducing greenhouse gas emissions by at least 55% by 2030 and achieving net zero emissionsby 205017.

Amundi Global Bioenergy ESG Screened UCITS ETFManagement fees 0.35%*

Amundi MSCI New Energy ESG Screened UCITS ETFManagement fees 0.60%*