Fixed income

‘Higher for longer’ doesn’t mean ‘higher forever’. Central banks are likely to be done with rate hikes as inflation decelerates and global growth stalls. The Fed has indicated to likely cut rates in 2024.

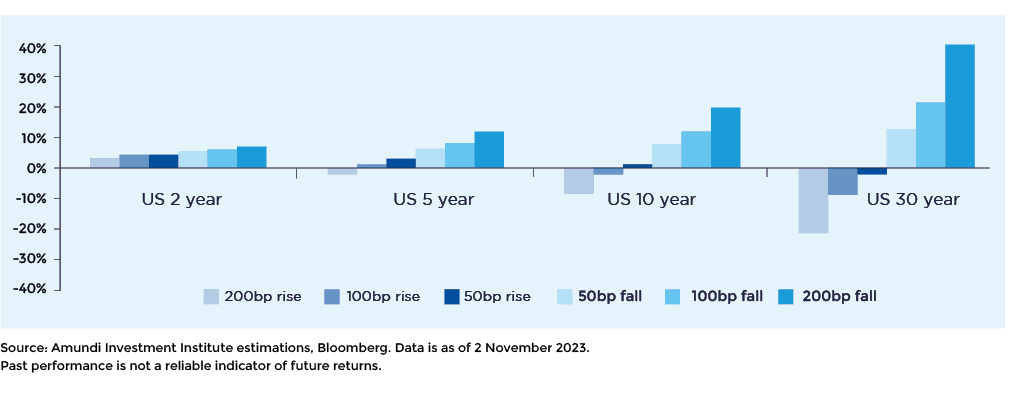

With interest rates having risen during 2023 to curb inflation, investors found value in shorter-dated bonds to help defend their portfolio.

But with rates peaking - or having peaked - adding duration is key to locking in higher levels as longer-dated bonds are the biggest beneficiary of falling rates.

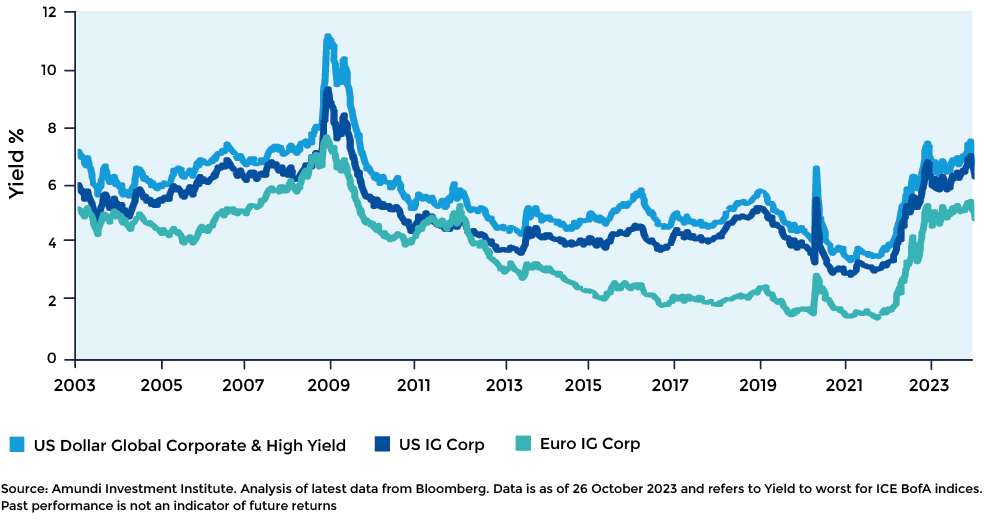

US Treasury valuations are attractive in light of a weaker macro backdrop. The Fed has been more aggressive with its policy rate hikes compared to the ECB. As a result, US fixed income currently offers more attractive yields compared to European markets.

12-month total returns with different yield movements over 1 year horizon

Outlook: Growth is slowing, inflation is coming down and these trends are likely to accelerate in 2024. Investors will need to add duration to their portfolios in early 2024.

Preferences: Consider US Treasuries (UST) and EUR government bonds for the potential of steady income with lower risk.

With the Fed seemingly done with its tightening cycle, attention is turning to the timing of its first rate cut. We anticipate that the current high-rate environment will push the US economy into a shallow recessionary phase in the first half of the year. On this basis, we anticipate better performance from US Treasuries and keep a positive stance.

US government bond yields are also an indication of potential further downside in the US dollar. A currency-hedged allocation to US Treasuries could allow international investors to reduce the volatility of their exposures.

With EUR bonds, we enter 2024 with a neutral stance on duration in light of the ECB’s data-dependent approach on inflation, and stand ready to increase duration through 2024 depending on the inflation path.

We expect the ECB to be done with rate hikes, with Christine Lagarde acknowledging that the “effects of monetary policy are already more forceful than expected” even if the Governing Council “did not discuss rate cut at all” so far. The ECB will remain cautious and fully reinvest securities under PEPP9 through the first half of 2024, bringing some support to the government bond asset class.

Core government bonds are currently attractive and adding duration will be key as the growth picture likely deteriorates. But lower-rated sovereign debt is likely to face stress as economic conditions worsen, so we remain cautious on peripheral issuers.

Amundi Euro Government Bond 5-7Y UCITS ETF Management fees 0.165%*

Amundi Euro Government Tilted Green Bond UCITS ETFManagement fees 0.14%*

The expected economic slowdown, together with the assessment of absolute valuations and technicals, supports the case for focusing on quality in credit markets, with a preference for Investment Grade (IG) credit.

Although fundamentals within IG show some deterioration, credit metrics still look sound from a historical perspective, with margins supported by higher pricing power and lower input costs, which are preventing leverage from rising as has occurred in some previous cycles.

The impact of monetary tightening on corporate fundamentals has been limited so far, owing to the significant liquidity accumulated during the Covid-19 crisis and low short-term refinancing needs.

However, the transition towards higher funding costs will be more painful and faster for low HY-rated corporates, which have less ability to generate cash flow, are more vulnerable to higher short-term refinancing needs and are more sensitive to the strong repricing in bank loan costs.

The most indebted leveraged companies may face the risk of default and a gradual increase in default rates is anticipated. S&P Global Ratings reported 25 defaults in the year leading to the end of November, which compares to 17 over the same period last year.10 This is well above historical averages.

Corporate bond valuations look attractive at absolute levels and continue to attract positive flows, primarily in the high quality/IG space, thanks to the attractive trade-off between the yield offered and resilient credit quality.

Technicals also look more favourable for IG than HY on the demand/supply balance. Primary markets are likely to keep showing healthy activity in the IG sector, although without pressure being too strong in terms of net issuance versus the past.

Amundi US Treasury Bond 7-10Y UCITS ETFManagement fees: 0.05%*

Amundi US Treasury Bond Long Dated UCITS ETF Management fees: 0.07%*

Outlook: Slowing economic conditions will impact corporate fundamentals and support a case for higher-quality credit over high yield.

Preferences: Focus on quality credit through US and Euro Investment-grade credit.

H1 2024

H2 2024

2025

Amundi Index US CORP SRI UCITS ETFManagement fees 0.14%*

Amundi index Euro Corporate SRIUCITS ETFManagement fees 0.14%*

Amundi EUR Corporate BondUCITS ETFManagement fees 0.07%*