Equities

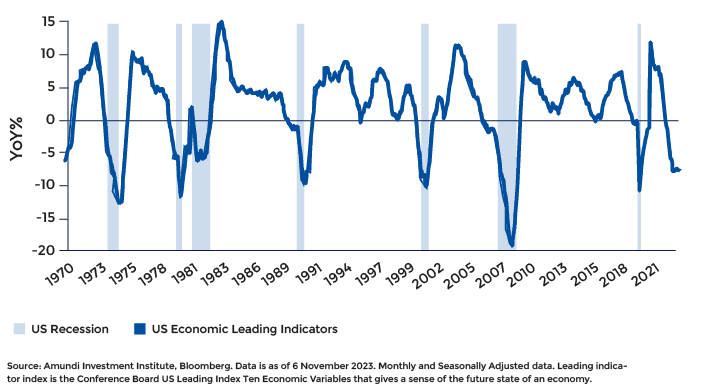

History shows that when Fed rates plateau, equities only tend to rise if there is no recession ahead or if a stock-market bubble is building. Otherwise, after some resistance, equities generally decline.1

Our anticipation of a mild recession materialising in the first half of 2024, and the overvaluation of some US stocks (Magnificent 7)2, point to this second option and we believe that revisiting the lows of October 2022 is a distinct possibility for MSCI World in the first half of the year.

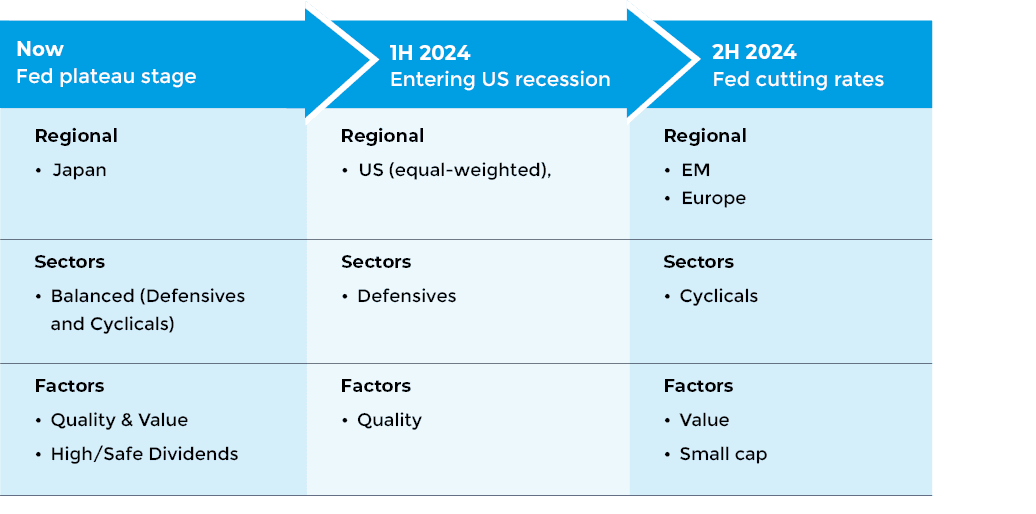

Outlook: Slowing global GDP and weakening fundamentals point to a challenging outlook for developed market equities entering 2024. Investors should consider a defensive profile entering the year and then picking up cyclical exposures again when the Fed implements rate cuts.

Preferences: Consider US equal-weighted (to avoid concentration risk), and Japan. US small caps may benefit from a probable Fed Pivot later in the year. In Europe, look at safe dividends, Quality and Value. Later, as the economic direction becomes more clear, consider sector rotation.

In this context, investors may wish to consider shifting from a balanced to a defensive profile entering 2024 and only turn towards cyclical markets again when the Fed implements rate cuts.

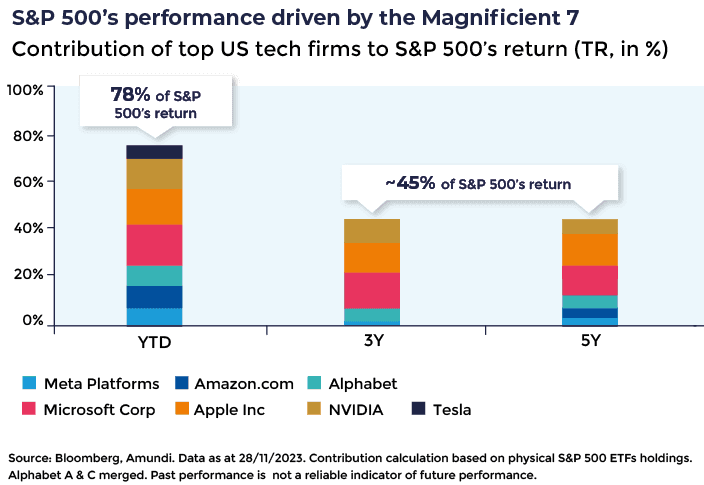

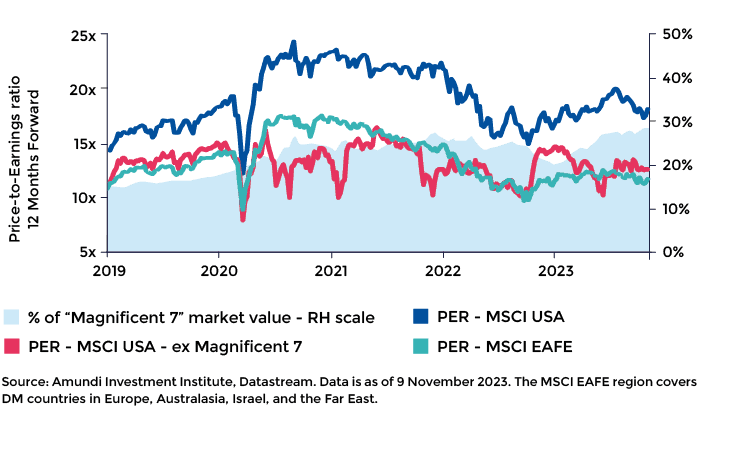

US:In US equities, we are witnessing a dichotomy where valuations and earnings potential in some segments are high versus others which appear overvalued. For instance, mega cap valuations are extreme, but outside these, equal weighted indices have not risen so strongly.

Investors seeking a more defensive exposure to US equities may therefore wish to consider equal-weighted indices as an alternative to traditional market capitalisation-weighted indices. These offer greater diversification, and may carry less risk, an approach that can be particularly beneficial when indices are heavily skewed towards their top holdings, such as at the present time.3

Small and mid caps may also be worthy of consideration later in the year: they show more reasonable valuations and may benefit from a probable Fed Pivot in the coming months.

Management fees: 0.18%*

Management fees: 0.35%*

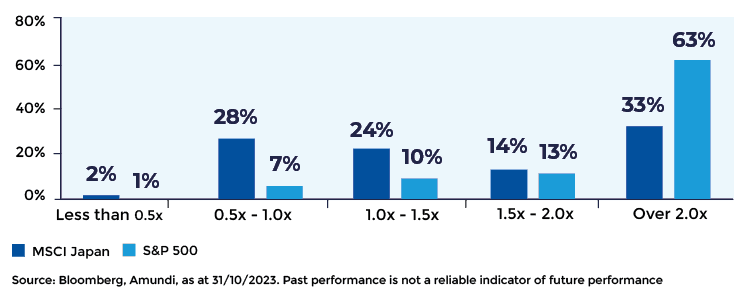

The land of the rising sun may be a good entry point. Japanese equities have performed well over the past year and appear to have regained international investors’ favour. The local economy has been supported by a recovery in domestic demand, an accommodative central bank and regulatory steps to improve corporate governance. This, along with still attractive valuations compared to other developed markets, supports the case for a neutral stance on the market.

Distribution of PBV by index constituents (in % of total constituents)

Management fees: 0.12%*

Management fees: 0.45%*

Lyxor Core STOXX Europe 600 UCITS ETF Management fees: 0.07%*

Amundi Index MSCI Europe ESG Broad CTB UCITS ETFManagement fees: 0.12%*

Amundi European Factor ETF RangeManagement fees: from 0.23%*

Amundi Global ESG Sector ETF RangeManagement fees: from 0.18%*

When the Fed rate cuts do finally materialise this should then favour undervalued European equities. For now, within factors we believe safe dividends are worthy of consideration and favour corporates with high payout policies as these tend to have sustainable and relatively predictable cash flows.

As consumers’ real incomes come under pressure, the pricing power of companies is also likely to be tested. In this context, we believe quality companies with strong balance sheets, high pricing power and high margin levels can more easily pass on rising input costs and may be better positioned to outperform. Favouring these companies can help build portfolio resilience against inflation and recession. Value also remains in focus.

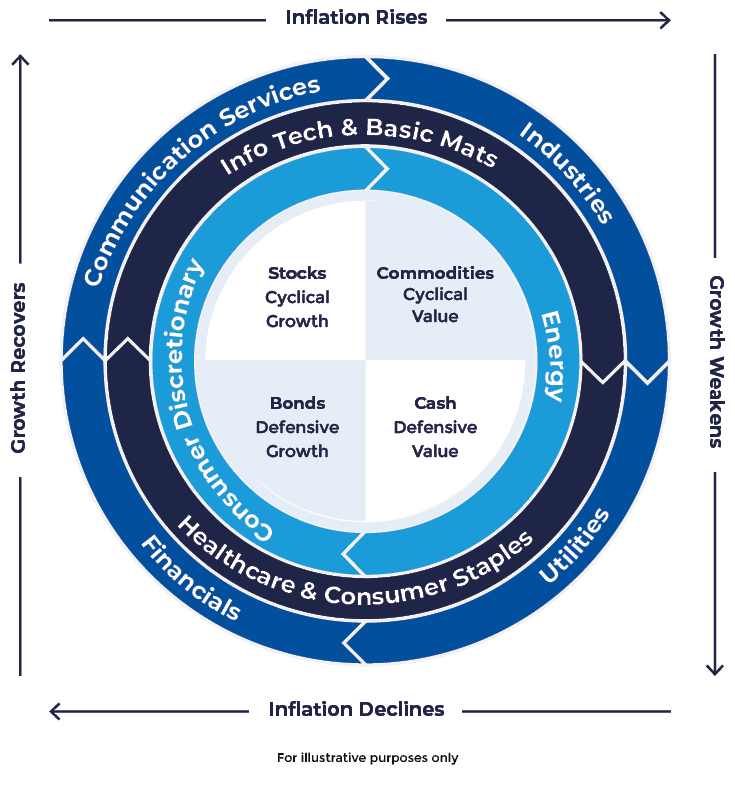

Consider sector rotation: In an environment of slowing growth we believe investors should start the year with a defensive stance, favouring Healthcare and Staples, and adding Utilities and Telecommunications as bond yields fall further. Later in the cycle, when monetary policy starts to reverse, consider reallocating to cyclical sectors such as Financials and Consumer Cyclicals.

Yes

No

Not Sure

Amundi MSCI China Tech ESG Screened UCITS ETF Management fees: 0.55%*

Amundi MSCI Emerging Ex China ESG Leaders Select UCITS ETFManagement fees: 0.35%*

Amundi MSCI Emerging Markets II UCITS ETF Management fees: 0.14%*

Amundi Index MSCI Emerging ESG Broad CTB UCITS ETF Management fees: 0.20%*

Amundi MSCI EM ASIA UCITS ETFManagement fees: 0.20%*

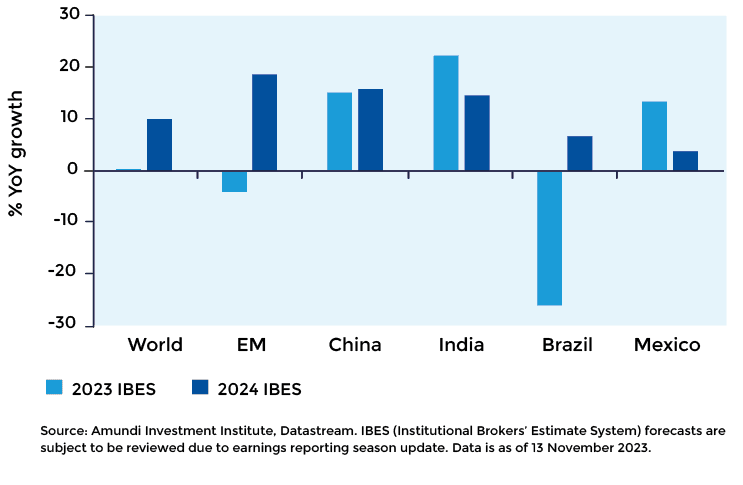

Although China’s post-Covid recovery has stuttered, EM at large has been resilient. EM GDP growth for 2023 was driven by India, Mexico and Brazil.4

Another factor that has impacted EM equities’ performance has been the strength of the US dollar over the past decade.5 A strong dollar often leads to tighter credit conditions (due to dollar financing) and drives inflation higher in these economies. With the Fed now likely done with rate hikes, the dollar is likely to continue its progressive downtrend, a positive factor for EM equities’ performance.

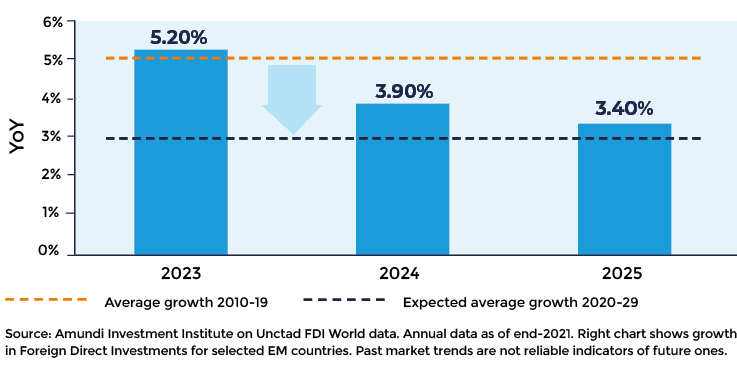

While a broader softening of EM growth is expected in 2024, it is unlikely to spiral into a general recessionary scenario and a mild recovery is anticipated by mid-year. Growth in EM is expected to decelerate to 3.6% on average from around 4.1% in 20236.

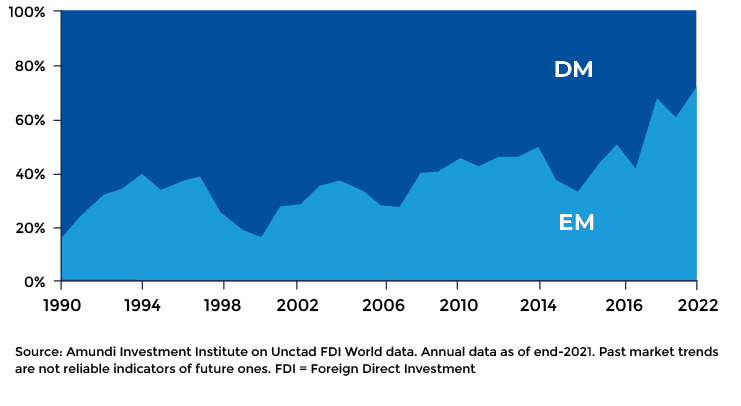

Importantly, the growth premium in favour of Emerging Markets over Developed Markets is projected to continue widening. Asia is set to register the strongest contribution to world GDP once again.

Beyond the cyclical downturn, there are structural factors at play that support EM. These factors include an incrementally higher global fragmentation, involving a great reallocation, near/friend-shoring, supply chain de-risking as well as the need for critical materials for the net zero transition, which are largely sourced from EM economies.

In our view, large divergences are likely to persist in EM equities. We maintain a neutral stance on Chinese equities for now in anticipation of further bouts of volatility in the short term as policymakers engineer China’s shift from an export-oriented market to a more domestic consumption-led economy less reliant on debt.

At the same time, China leads the manufacturing and trade of clean energy technology, an area of specialism that investors should consider in their asset allocation.

We do, however, expect China’s economy to grow just below 4% in 2024 with mini monetary easing, and a 20bp rate cut likely in H2 2024. Taking these factors into account, along with the complexity of the local market, there is a case for adopting a separate allocation to China from the EM bloc.

Outlook: Emerging Markets (EM) have proven resilient but with higher fragmentation. We hold a positive view with a focus on structural themes in Asia (internal demand, supply chain relocation) and valuations in Latin America (LatAm).

Preferences: Within EM, consider Asia – in particular China – as a “winner” on technology disruption, and an EM-ex China allocation; additionally consider adding LatAm and more specifically Brazil to EM portfolio selection.

LatAm performed well in 2023 due to attractive valuations and better-than-expected GDP growth. Inflation dynamics have improved in the region, and lower inflation allowed local central banks to start easing policy rates in the summer.7 Looking ahead, further easing is likely, which should eventually support underlying activity.

Valuation levels in the region remain attractive versus historical levels and against other EM economies. Delving further into LatAm, Brazil surprised to the upside in 2023. The local market’s outperformance has been driven by its strong exposure to the materials and energy sectors with higher commodity prices supporting local equities.8

In 2024 we believe this country could benefit from a cyclical improvement in earnings per share and could emerge as a potential winner in the energy transition from commodities and biomass production.

Amundi MSCI EM Latin America UCITS ETF Management fees: 0.20%*

Amundi MSCI Brazil UCITS ETFManagement fees: 0.65%*