Introduction

What we already know about 2024 is that it will be a year of celebration at the Paris Olympics, of reflection on the 80th anniversary of D-Day, and of ambition with audacious space missions preparing for lift off.

For ETF investors, though, the key consideration will not be about ‘take-off’ but instead the landing point for the global economy. Interest rates are peaking, inflation is moderating and the growth outlook is fragmented, but broadly slowing.

These turning points in growth, inflation and monetary policy may generate opportunities for investors to rotate from a more defensive to a more constructive stance during the year.

Explore our outlook for ideas of what to expect on the financial markets in 2024. In addition, discover where opportunities may be found through an ETF implementation.

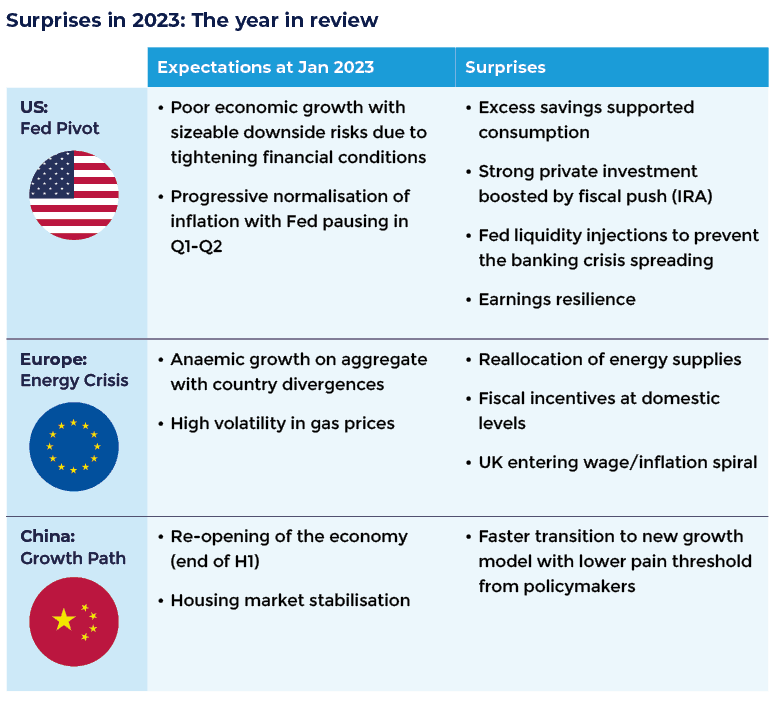

As we entered 2023, the path of inflation was in focus, along with concerns about energy prices in Europe, and China’s reopening following strict lockdown measures during the pandemic.

As ever, 2023 presented a few surprises such as the resilience of the US economy and the UK’s wage-price spiral.

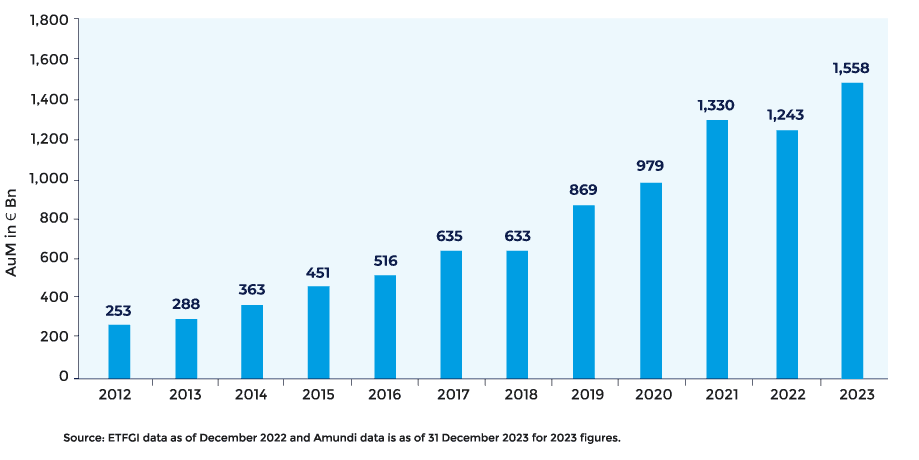

The European UCITS ETF market experienced strong growth in 2023 with assets under management (AuM) reaching €1,558 billion at the year end versus €1,243 billion in 2022.

Flows proved robust in a challenging market context in which central banks across the globe pursued one of the fastest tightening cycles on record in a context of elevated price levels.

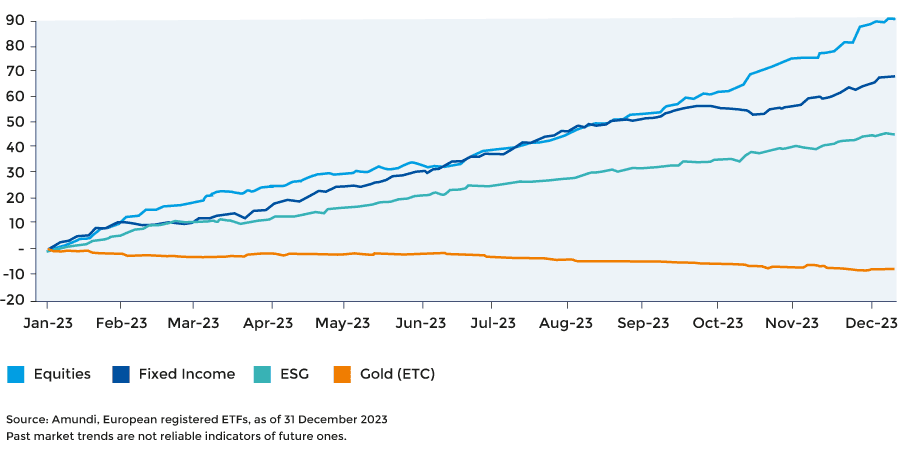

The rotation towards ESG remained strong in both equities and fixed income across the year. Net New Assets (NNA) reached €45 billion. Overall, ESG ETFs accounted for 29% of total inflows in European ETFs.

Total ESG ETF AuM in Europe continued to increase in 2023, standing at over €349 billion at the year-end and representing almost 22% of the total size of the European ETF market.

At the beginning of 2023, investors were still in neutral mode but this transitioned to a more opportunistic stance, notably towards allocation into US Equities. After a volatile start to the year, US equities’ performance was driven by a strong recovery of technology and growth stocks supported by the breakthrough of AI and machine learning technologies.

NNA reached €90.3 billion at the year-end versus €54 billion in 2022. Flows into Europe equities were limited (€6.2 billion) with investors lacking upside catalysts for a strong allocation into local equities at a time of anaemic growth and still elevated price levels.

Elsewhere, World, US, Emerging Markets and All Country equities exposures gathered stronger inflows. Of note also was the strong reversal from a positive momentum to significant outflows in the second semester of investors’ allocations into China equities.

High interest rate levels was the dominant theme in 2023, and pretty much all segments benefited from strong investor appetite for fixed income. In fact, 2023 was a record year for inflows into fixed income ETFs, which gathered €61.5 billion in net new assets across the year. The asset class presents attractive options for seeking investors and those looking for total return, particularly after more than a decade of low interest rates.

During the first two quarters Investment-Grade Corporate Bonds in Euro and US Dollar curried the most favour among investors. However, a shift in investment preference has materialised since September. Investors allocated heavily into US Treasuries and Euro Government Bonds to get exposure to fast decreasing long term interest rates. This came on anticipations that policy rates from major central banks have peaked.

Throughout the year, Euro and US Government bonds gathered €16.7 billion and €15.4 billion in net new assets respectively, whilst Euro Corporate bonds enjoyed €11.4 billion of inflows.

The gold price recently reached its highest level since May as investors assessed how the crisis in the Middle East might impact the global economy. Yet the rebound in the gold price has not been reflected in investors’ positioning. Total known ETC holdings of gold hovered around historical lows at the year end.

Type your content here…

Macro views: Slowing growth and inflation expected for 2024

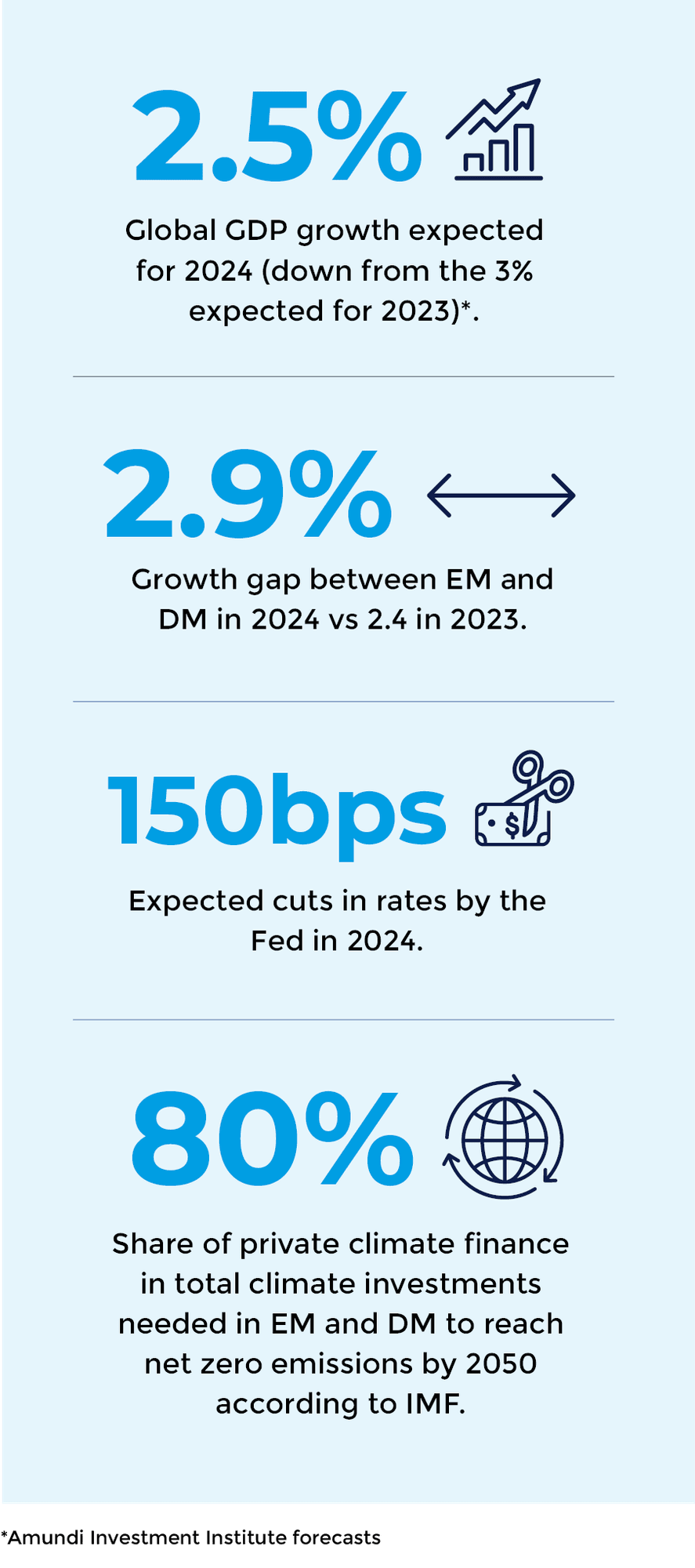

For investors thinking about 2024, inflation remains a focus area, even as the economic growth outlook is fragmented. A gradual weakening of global growth is expected. Inflation will probably slow but is likely to remain above central banks’ targets. Other dynamics that investors should keep on their radar include energy costs and corporate default rates, among others.

In this fragmented world, a recession is expected in the US in the first half of the year as higher rates bite, though inflation could move closer to target in the second half of the year. For the Eurozone, growth will likely remain low amid more restrictive fiscal policy on top of tight monetary policy.

Growth in Japan will start to decline but is likely to stay above trend, while a structural shift is underway in China towards more sustainable but lower economic growth. Emerging markets look to be more resilient overall.

National elections may impact the markets as investors consider what the elected representatives may mean for a specific country’s direction, and what that could mean for overall market performance.

This year, several crucial elections are scheduled, which could have far-reaching effects for investors. Both Russia and Ukraine go to the polls, as will India, the world’s largest democracy by population. And later in the year, Brits and Americans will have the opportunity to cast their votes.

High stakes elections will shape 2024

Taiwan

13 January

Russia

17 March

Ukraine

TBD

India

Likely Q2, TBD

Mexico

2 June

EU Parliament

6-9 June

US

5 November

Venezuela

South Africa

UK

Likely Q4, TBD

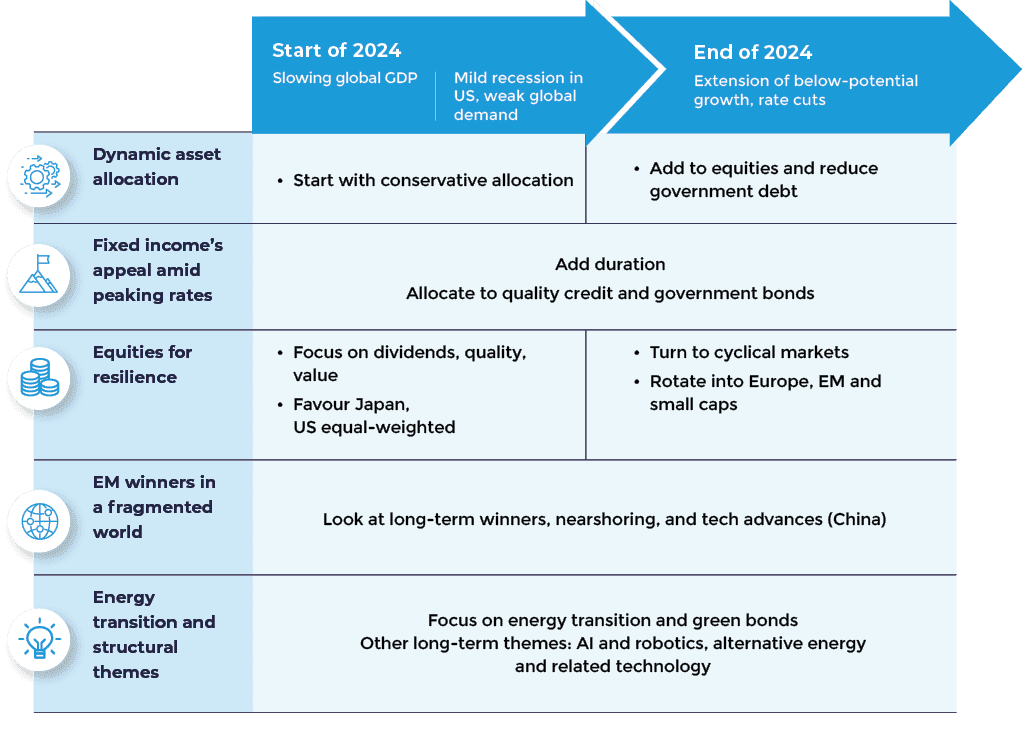

Investment opportunities: start defensively, then turn constructive

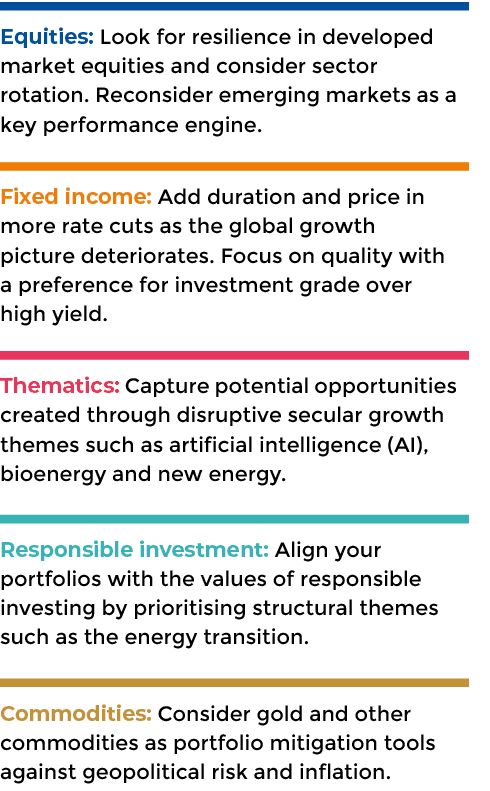

With these scenarios in mind, our view is that fixed income should play a crucial role in portfolios at the start of the year, through government bonds (with added duration) and investment grade credit.

In equities, investors should consider opening 2024 defensively with a focus on dividends, quality, and value as well as US (equal-weight exposure) and Japan, before turning to cyclical sectors and rotating towards Europe and emerging markets (EM) when the Fed starts reducing policy rates. EMs should be a key pillar in 2024 and beyond, with opportunities in Asia and commodity-rich countries such as Brazil, which are increasingly instrumental the green transition. Investors cannot ignore responsible investing: While the energy transition a focus, other themes are gaining traction and could deliver long-term value.Our outlook assumes that energy prices will remain contained and that geopolitical risks will be confined to specific regions. Gold and other commodities remain a solid risk mitigation tool.