The case for a government bond allocation

Marketing Communication

While no investment can be risk-free1, some could be considered less risky than others, which is worth taking in mind when you consider your portfolio construction.

It is, after all, better to stick to the speed limit and to wear your seatbelt when driving a car. You could still get into an accident, but certain safety measures could help to mitigate any negative consequences. When it comes to investing1, certain types of assets could be considered to be something akin to a seatbelt.

Government bonds are often viewed as one such option that could help you meet long-term financial goals, because they could offer relative stability across a range of market environments.

First, it is important to understand what these assets are and how they work.

The starting point is this: Governments use bonds to borrow money for state spending. When you buy a bond from a government, you’re effectively lending it money. In return, you receive a fixed interest payment (the ‘coupon’) in each year of the bond’s lifetime. And at the end of the bond’s life – when it ‘matures’ – you get back the money you invested (the ‘face value’).

Together, the coupon and the face value are used to calculate a bond’s yield2: the gain you could make each year if you reinvest all the coupons until the bond matures.

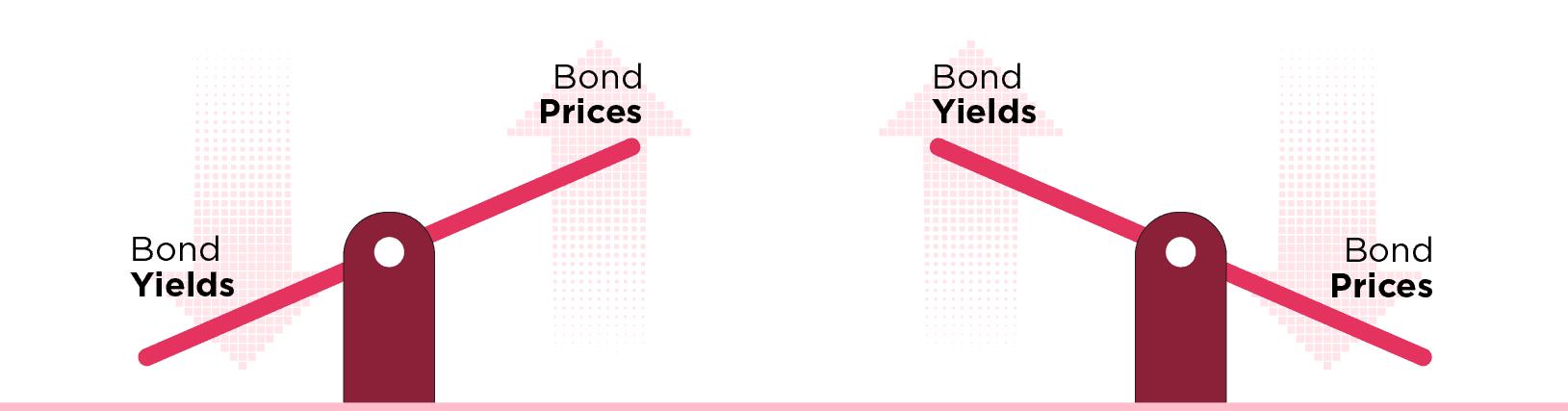

Of course, government bonds aren’t only bought and sold when governments issue them. There’s a huge secondary market, where prices rise and fall according to demand. This means that bond yields1 change with the prevailing market conditions: the coupons stay the same, but they become larger or smaller as a percentage of bond prices as those prices fall or rise.

Bond yields are especially influenced by changes to interest rates. Yields rise in response to higher rates and fall when rates will be lower. That’s because bonds would be less attractive investments if bank deposits offered better returns.

Source: Australian Federal Reserve, Amundi ETF. For illustrative purposes only

One of the main attractions of government bonds is their relative stability.

As government defaults (failure to pay coupons) are almost unknown in developed markets3, government bonds could be viewed as a useful building block in your portfolio.

For investors in government bonds, some of the most important assets are generally seen as US Treasury bonds, UK gilts and euro-area bonds – which include German bunds, and French and Italian government bonds.

Rating agencies provide ratings evaluate a country’s ability to repay its debt, which they base on numerous parameters including economic conditions and fiscal policies. Government bonds, especially those with good credit ratings, could be a useful complement to more volatile assets such as equities – providing vital diversification4 in portfolios.

Sometimes, stocks and bonds rise or fall together. But the two asset classes often respond to events in different ways.

When the outlook looks uncertain or when geopolitical developments cause panic, bond prices often rise2 as a result of a ‘flight to safety’ even as equities decline.

Credit Risk Level

Credit Ratings (Moody’s/ S&P/Fitch)

Description

Examples

Low

Aaa / AAA / AAA

Very low risk of default; stable economy

United States, Germany, Switzerland, Japan

Medium

Baa / BBB / BBB

Moderate risk; some economic or political concerns

Spain, South Korea, Brazil

High

Ba and below / BB and below / BB and below

Higher risk of default; economic or political instability

Argentina, Venezuela, Nigeria

Source: Amundi. Data as of end-September 2025. For illustrative purposes only. May change without notice.

For investors in government bonds, some of the most important assets are generally seen as US Treasury bonds, UK gilts and euro-area bonds

When allocating to government bonds, there are two broad considerations. The first is the portfolio’s strategic asset allocation – the long-term target levels of its bond holdings. Here, the time horizon is typically 10 years.

The second is its tactical asset allocation – the short-term adjustments that an investor might make based on economic conditions, interest rates and so on. This is a much more opportunistic consideration based on market trends.

One risk with government bonds issued by different countries is that currency movements could reduce or even erase returns5. For example, if the dollar weakens against the euro, returns from US Treasuries would be worth less in euro terms – so European investors could lose out. This matters because it could disrupt the otherwise stable returns6 from government bonds.

To get around this, currency-hedging strategies could be a consideration. In its most basic form, ETF issuers might offer a government bond solution that is hedged: For example, a US dollar government bond product that is ‘hedged’. By using these instruments, investors could translate bond income into their own currency at a pre-determined exchange rate – thereby limiting the potential impact of currency fluctuations.

Amundi’s range of bond ETFs are designed to offer a suite of solutions to suit different risk appetites and market cycles. When you invest in an ETF, you outsource all of the complexities of bond investing – allowing you to concentrate on the overall shape of your portfolio construction.

Explore Amundi’s government bond ETFs

1 Investment involves risks. For more information, please refer to the Risk section below. 2 Yields are not guaranteed.3 Past market trends are not a reliable indicator of future ones.4 Diversification does not guarantee a profit or protect against a loss.5 Past performance is not a reliable indicator of the future ones.