Hit the ground running: The case for goals-based investing

Marketing Communication

When preparing for a marathon, a runner will tailor their training to their lifestyle, personal commitments, risk of injury, and time targets. They will increase their mileage through the training plan and then taper, or reduce, the distance they run in the last couple of weeks to minimise the risk of injury and to ensure fresh legs for the big day. Long-term planning is crucial.

As investors get closer to their target investment date, the portfolio becomes more cautious - much like a marathoner tapers their mileage closer to marathon day.

A runner’s training programme has a lot in common with an investor’s approach to goals-based investing. At heart, goals-based investing is driven by personalisation, with investors encouraged to define their objectives right at the start of the journey.

Some goals-based investing strategies are designed to automatically adjust asset allocation based on personal goals, time horizons and risk tolerance. As investors get closer to their target investment date, the portfolio becomes more cautious - much like a marathoner tapers their mileage closer to marathon day.

For illustrative purpose only

Unlike traditional investing1, which is largely based on chasing returns or trying to ‘beat’ the market2, goals-based investing is all about aligning your investment strategy with personal aspirations. It’s a marathon, not a sprint, as they say.

The first step in goals-based investing is to clearly define financial goals and whether they are short-term, long-term, or something in between.

This clarity transforms the investment process from a mere numbers game into a more purposeful journey towards achieving a desired outcome. By focusing on specific goals instead of just returns, investors can consider tailored strategies that reflect their unique requirements.

Goals-based investing could potentially deliver a more level-headed approach to monitoring investments. Research shows that when an individual can visualise their financial goals, they may be more motivated to adhere to their investment plans, even when the road ahead may be challenging3.

Goals-based investors are encouraged to reflect more holistically on their broader financial plan.

The greater or more important the goal, so the thinking goes, the less likely investors are to fall foul of making impulsive decisions when the markets are volatile4. In much the same way, those running 42.2km need to keep a consistent pace and resist the temptation of running too fast and depleting their energy stores, or of quitting when the going gets tough.

A marathoner must also think about more than just their legs. Replenishing sugar levels and ensuring adequate hydration are essential. Similarly, goals-based investors are encouraged to reflect more holistically on their broader financial plan, taking into consideration income, expenses and other personal responsibilities.

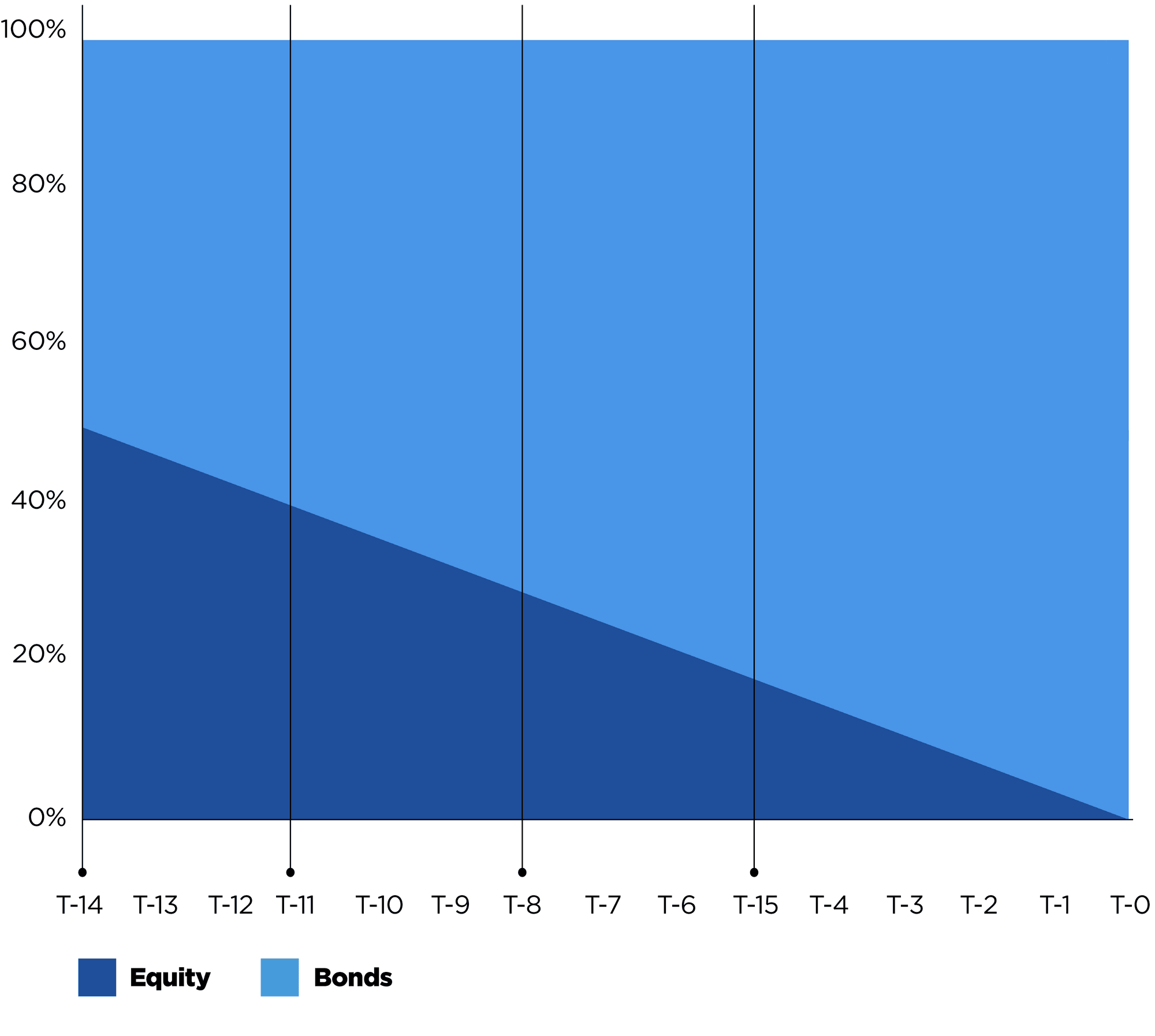

Investments that reallocate assets to reduce risk over time often use what is known as an investment glide path. This is a predefined strategy that reduces the proportion of equities and increases that of bonds over time as an investor’s risk profile changes (equities are generally more risky than bonds, although bonds are not risk-free1).

In the ‘glide path’ chart, you can see that the strategy starts with a large equity allocation (T-14), which reduces over time, while the proportion of bonds increases as the target date (T-0) nears.

Source: Amundi ETF, as of 29/04/2025. For illustrative purposes only.

Goals-based investing is all about setting specific targets, being clear on what your time horizon is and then making adjustments based on your evolving approach to risk. Amundi ETF offers several goals-based investing strategies that could suit your needs.

1 Investment involves risks. For more information, please refer to the Risk section below.2 "Beating the market" refers to the ability of an investor to achieve returns that are higher than a benchmark index.3 Journal of Financial Counselling and Planning, Volume 31, Number 2, 2020.4 Building a Practically Useful Theory of Goal Setting and Task Motivation, Edwin A. Locke and Gary P. Latham, the American Psychological Association, 2002.

At the start, a Lifecycle ETF combines a collection of stocks and bonds to drive potentially higher returns1, but as investors get closer to their target date, the allocation becomes more cautious5.

Learn more about Lifecycle ETFs

A fixed maturity ETF aims to replicate the performance1 of a group of bonds with similar maturity dates. It offers clear visibility of the estimated yield you will receive right from when you first invest6.

Explore fixed maturity ETFs

Also known as a capital accumulation plan, or savings plan, this is a method of subscribing to funds, including ETFs. Available in certain markets, it allows you to invest predetermined instalments for a given period of time.

5 By rebalancing the portfolio to hold more fixed income and less equities, for example. 6 Estimated yield: This is the yield that would be realised on the ETF if it were to be held to its maturity date. Please note that the yield to maturity is not guaranteed.