Fixed income ETFs and the economic cycle: Striking a balance

Marketing Communication

Why investors might consider ETFs for fixed income strategies

Investing in fixed income through exchange-traded funds (ETFs) has several advantages. ETFs can be bought and sold on the stock exchange in the same way as equities. Also, they enable investors to achieve a level of diversification2 that would be difficult and expensive to achieve through buying individual bonds.

The fixed income universe can look like a complicated place. Yet it is worth trying to build a deeper understanding of the bond market because these assets could help broaden your investment portfolio, potentially improving long-term performance and reducing risk1.

Considered less risky than equities, though not risk free, bonds are issued by governments, companies and other entities. These are bond issuers. Bond investors, or bondholders, are essentially lending money to these issuers. In return, investors typically receive a fixed interest rate from an issuer, hence ‘fixed income.’

Demystifying fixed income terminology

COUPON - The fixed amount of interest a bond pays its holder.

YIELD - This is a variable return that an investor could receive each year. It is influenced by factors like the bond’s market price and interest rates.

MATURITY - The date at which a bond issuer must repay the original bond value to the bond holder.

Different types of bondsThe two most common types of bonds by issuer are:

Government bonds issued by national governments.

Corporate bonds issued by companies.

Corporate bonds can be divided into two categories based on credit quality3:

• Investment grade corporate bonds which are issued by companies viewed as carrying a lower level of risk4.

• High-yield corporate bonds are those that are seen to be riskier but that tend to have higher yields5 to reflect this increased risk.

Government bonds usually carry the lowest risk and generally have the longest maturities. However, their long maturities mean they can be more sensitive to changes in interest rates. In contrast, the yields on high-yield bonds tend to be more dependent on company- or sector-specific factors.

Market cycles can significantly impact interest rates and, consequently, bond performance

Bond performance through the market cycle

It’s important to understand how a bond’s performance can vary in different economic conditions, particularly when interest rates are rising or falling.

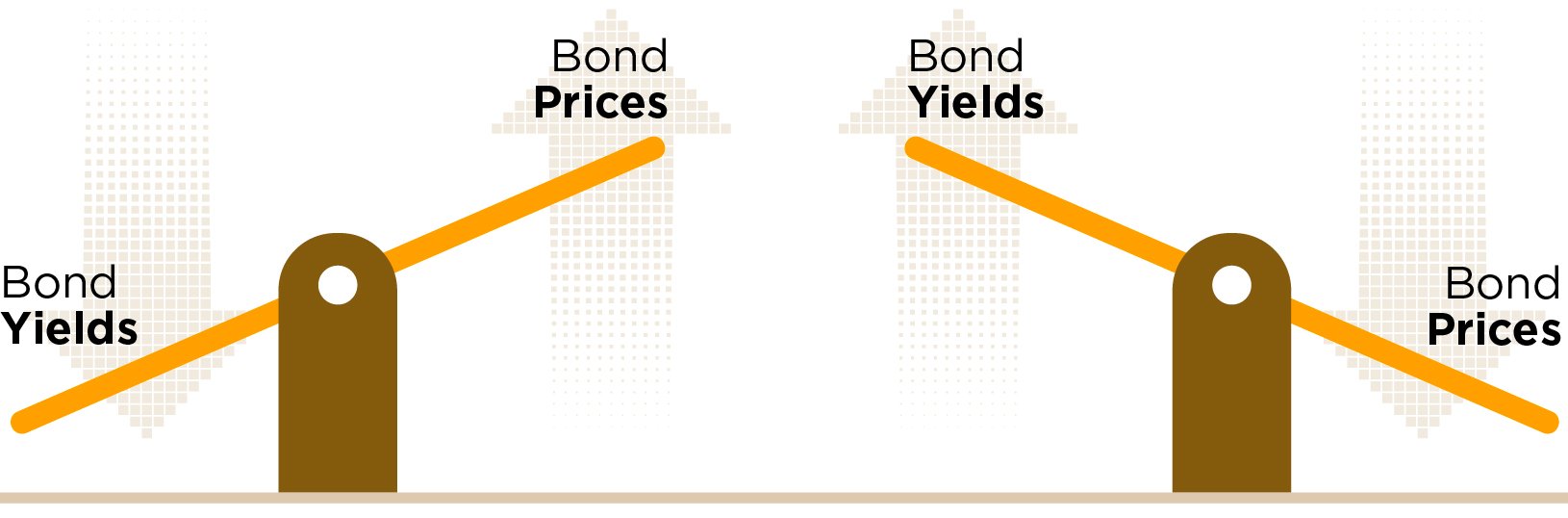

When interest rates rise, bond prices typically fall and yields rise. This happens because new bonds are issued at higher rates, making existing bonds with lower rates less attractive. Conversely, when interest rates fall, bond prices usually increase with yields also falling. Investors are willing to pay more for existing bonds that offer higher interest payments compared to new bonds issued at lower rates.

Market cycles can significantly impact interest rates and, consequently, bond performance. During economic expansion, central banks may raise interest rates to control inflation, leading to declining bond prices. In contrast, during economic downturns, central banks often lower interest rates to stimulate growth, which can boost bond prices.

You might also consider the duration of bonds, which measures their sensitivity to interest rate changes. Longer-duration bonds tend to be more affected by interest rate fluctuations than shorter-duration bonds. Therefore, investors should assess their risk tolerance and investment horizon when choosing fixed income investments.

By keeping an eye on interest rate trends and economic conditions, investors could make more informed decisions that align with their financial goals.

Investors should assess their risk tolerance and investment horizon when choosing fixed income investments

Source: Australian Federal Reserve

How different types of bonds are impacted by the economic cycle

Government bonds• The lower-risk nature of bonds issued by governments – especially in developed markets – means that, during periods of economic expansion, they will tend to underperform other bonds. • However, as the trading environment becomes more challenging, investors may turn to government bonds as they are considered safer assets, driving their prices up.

Investment grade bonds • These are often preferred in deteriorating economic conditions, because these assets are issued by robust companies with stronger balance sheets.• The investment grade rating therefore signifies a lower risk of default.

High-yield bonds • High-yield bonds tend to perform better when economic conditions are improving, when default rates are typically lower, and when overall financial resilience generally improves. • During periods of slowing growth and recession, high-yield bonds may suffer, as historically default rates rise and investors seek safer assets.

Floating-rate notes are another type of fixed-income investment that pays a variable rate of interest. This is typically linked to a benchmark such as the US Federal Reserve’s Fed Funds Rate, or interest rate. As central banks increase interest rates – often in order to bring inflation under control and stop economies overheating – returns on floating-rate notes will rise, and vice versa. However, floating-rate notes may perform relatively well when rates are cut if rates do not fall as quickly as investors expect.

How fixed income ETFs could help deliver consistent returns

Historically, bonds have tended to perform well at times when share prices are falling, and vice versa. This negative correlation between fixed income and equities means that owning both in a portfolio could help to deliver smoother, more consistent returns over the long term6. However, there is no guarantee that equity and bond prices will move inversely to each other.

At Amundi, we offer a wide range of fixed income ETFs, including government and corporate bond funds.

Explore fixed income with Amundi ETF

1 Past performance is not indicative of future returns.2 Diversification does not guarantee a profit or protect against a loss.3 Ratings agencies such as Moody’s, Fitch and S&P Global provide these credit risk ratings. 4 The risk in this case refers to the risk of the issuer defaulting, or failing to repay, money to investors.5 Yield is not guaranteed. Past performance is not indicative of future returns.6 Past performance is not indicative of future returns.