EU Commission objectives and new initiatives tackling indices

The Benchmark regulation was amended by the Low Carbon Benchmark regulation in December 2019.

The “level 1” of this new EU regulation introduced two major innovations:

The creation of two new categories of benchmark under the BMR – Climate Transition Benchmarks (CTBs) and Paris-aligned Benchmarks (PABs)

Disclosures requirements in terms of sustainability-related information for benchmarks administrators, with regard to their methodologies and ESG characteristics.

The so-called “level 2” final texts of July 17, 2020, commonly referred to as Regulatory Technical Standards (RTS), which specify how the new regulations have to be applied were published on December 3, 2020 and came into effect on December 23, 2020.

With the amendments to the Benchmark regulation, and by introducing binding legislation, the EU targets four main objectives[1]:

Increase the comparability of benchmarks, while leaving some flexibility to benchmark administrators when defining their methodology

Provide investors with an appropriate tool that is aligned with their investment strategy

Increase transparency on investors’ impact related to climate, notably climate change and the energy transition

Disincentivize greenwashing

[1] Source: EU Technical Expert Group on Sustainable Finance – “Final report on climate and benchmarks’ ESG disclosures” dated September 2019.

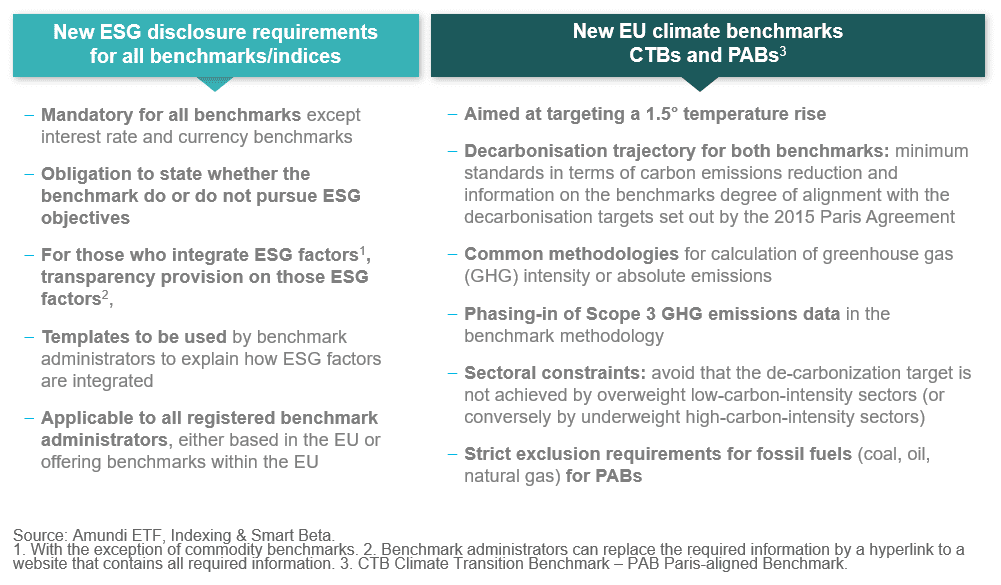

In line with the changes to the BMR, benchmark administrators are now required to publish ESG information related to all of their indices:

All indices, whether ESG or not, are in scope of the new rules. Interest rate and currency indices are the only exceptions.

For non-ESG indices administrators are required to clearly disclose that they do not pursue and ESG objective.

For ESG indices, it is necessary for administrators to clearly explain how ESG factors are integrated into each index or family of indices.

For each index, administrators must publish the methodology, the ESG characteristics of the index and how these are incorporated into the methodology using a template reporting. The information published is therefore standardised and comparable from one index to another.

As for all other benchmarks, and in relation to BMR requirements, the benchmark administrators of CTB and PAB indices must comply with a high level of transparency on their methodologies, through the formalised reporting accessible to investors.

This reporting is, however, much more detailed than that required for other indices. It includes:

Information on the methodology and data used (assumptions and precautionary principles, scenario upon which the GHG emissions objectives are made and the source of data for the calculations etc.)

Reporting on the decarbonisation strategy, and in the event that the objectives are not achieved, the reasons for this failure, as well as the means implemented in the following period to remedy the problem

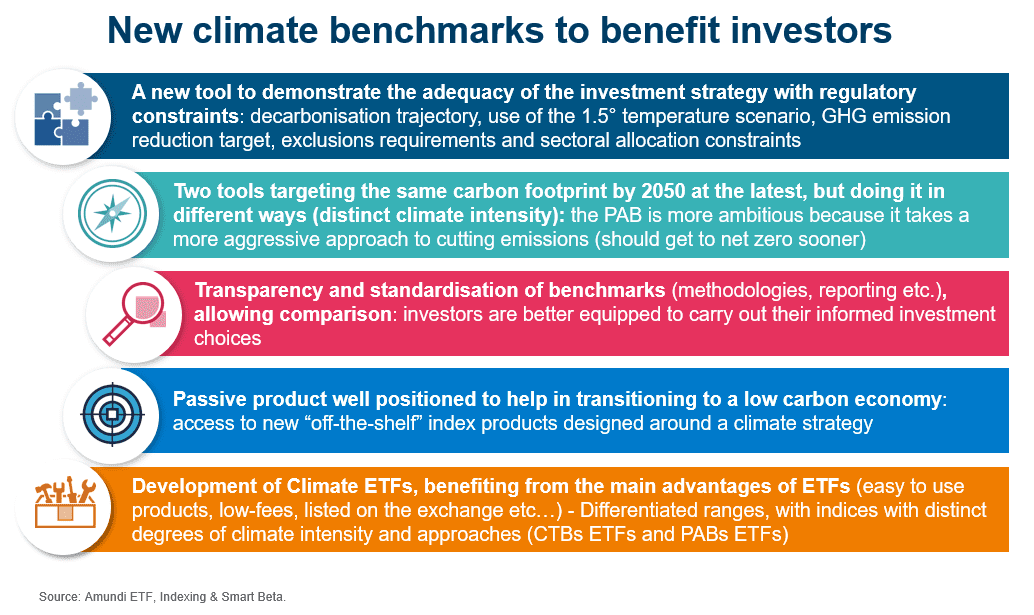

Importantly, the two climate benchmarks incorporate new attributes to allocate capital towards the most climate-virtuous companies:

They integrate a backward-looking approach, using reported historical data, and focus on Scopes 1, 2 and 3 upstream (supply chain for operations) and downstream (products) GHG emissions with an explicit allocation towards most climate virtuous companies

They take into account companies’ climate strategies over the long run and their forward-looking commitment towards carbon emission reductions

With the creation of the two new Climate benchmarks labels - "EU Climate Transition Benchmark" (CTB) and "EU Paris-Aligned Benchmark (PAB)", investors are able to align their investments with the objective of the Paris agreement. As stated by the EU Commission: “The two new categories are voluntary labels designed to orient the choice of investors who wish to adopt a climate-conscious investment strategy”.

These labels are the first European regulatory initiatives validated and adopted by the Union as a whole in the field of sustainable investment. They are the first European voluntary adoption labels, designed to guide investors interested in adopting a climate-friendly investment strategy.

This is obviously a strong message from the European Commission allowing for the pursuit of ambitious climate strategies, while all the other projects undertaken by the Commission are still ongoing. The new labels provide clear and transparent technical standards built by a panel of experts comprising industry practitioners, academics and NGOs (Non-governmental organizations).

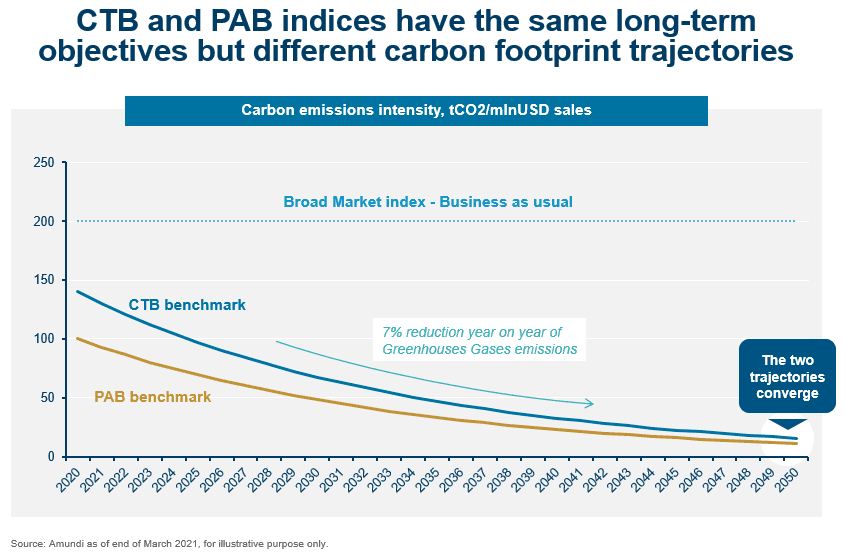

CTB and PAB benchmarks include important quantified objectives for decarbonisation (30% and 50% respectively). Funds based on CTB or PAB indices can meet the requirements to be classified as “Article 9.3” products under SFDR[1].

[1] A financial product that classifies as “Article 9” under SFDR is deemed either “Article 9.1” if it has sustainable investment as its objective or “Article 9.3” if it is a reduction in carbon emissions as its objective. An ETF whose underlying index is a CTB or PAB benchmark can be classified as “Article 9.3” under SFDR.

The two new climate benchmarks must comply with strict minimum requirements to achieve their climate objectives. The main constraints are defined as follows:

CTB

PAB

Reference temperature scenario

1.5° scenario with no or limited overshoot:

target of a 1.5° temperature rise

Year-on-year self- decarbonisation

At least -7% on average per annum since inception

Carbon intensity reduction vs parent investable universe

-30%

carbon footprint reduction

50%

Baseline exclusions

Companies involved in the following activities:

Controversial weapons

Societal norms[2] violators

Tobacco

And companies that significantly harm one or more of the environmental objectives[3]

Fossil fuel-related activity exclusions

No

Companies that derive of their revenues:

>1% of coal exploration/processing

>10% of oil exploration/processing

>50% of natural gas exploration/processing

>50% of electricity generation with GHG above 100gCO2e/kWh

Exposure to high climate impact sectors[4].

At least collectively equal to parent investable universe (no underweight)

[2] Societal norms: UN Global Compact and OECD Guidelines for Multinational Enterprises.[3] Article 9 of regulation 2020/852/EU (EU Taxonomy regulation): climate change mitigation, climate change adaptation, sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control, protection and restoration of biodiversity and ecosystems.[4] As defined under the European NACE sector classification system. Does not apply to Fixed Income indices.